Wise - 1H25 Key Takeaways

Stock Update - 1H25 Results

Wise reported a better than expected 1H25 result with underlying income rising 19% to £662.4m while underlying profit before tax (PBT) grew 57% to £147m. Gross margins were elevated at 76% from FX benefits (3%) and cost efficiencies (3%), which is expected to unwind in the 2H due to price cuts and reinvestment. This should see PBT margins of 22% gradually managed back towards its target range of 13-16%.

Investors continue to question the near-term financial visibility, primarily around guidance and margins. While this will be lumpy due to reinvestment and FX volatility, the real measure of progress should be on active customer and volume growth, which ultimately drives scale. The three result takeaways are:

Within a highly competitive market, delivering scaled economies shared is the best form of defence. Often the best form of defence is offence. Wise is returning scale benefits to continuously improve its price, infrastructure, product and service. This relentless focus delivers a superior customer value proposition, making it increasingly difficult for current and prospective players to compete.

Taking the inverse, if Wise were to stop investing today, we would see higher margins, stronger cash flows and a more predictable financial profile. However, the longevity of the business would be at risk, as the bar is lower for disruption. We have seen this in cross-border payments, firstly with banks and then with money transfer operators like Western Union. Through continuous improvement, Wise is derisking the business by increasing the barriers to entry.

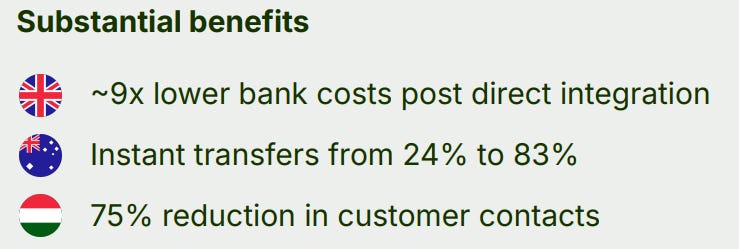

Infrastructure remains the foundation of Wise’s competitive moat. The company continues to enhance this by adding three new connections to local payment systems in the Philippines, Japan and Brazil. These milestones are significant, having built trust and scale over multiple years with central banks. In Japan, Wise is the first non-bank approved to join the Zengin payment system. The barriers are high to gain approval, while the benefits are material as seen below.

The result is Wise can significantly lower its cost to serve, reduce prices, and increase transaction speed—benefits that attract both individual consumers and large enterprises. The deal with Standard Chartered is a case in point, a major traditional bank that has decided to use Wise’s infrastructure to power cross-border payments in Asia and the Middle East. This is a watershed moment.

Capital allocation at Wise is disciplined with a focus on profitable returns. This is unlike many other FinTechs that seek growth at all costs. Wise’s new CFO Emmanuel Thomassin explains this, “we do have a lot of opportunities to invest that can bring the future closer, faster. We're totally looking into doing that. But as you've seen over the history and we want to make sure that every investment that we make is very clearly paying back in returns. And we’ve created the investment framework with a targeted level of profitability, which kind of gives us the bandwidth to invest ...I can confirm that these are really disciplined in terms of investments, which I really like. We are really focus on the return on the payback time, what should be accretive for the shareholders, what we invest here. So that's the case. We invest also long term. I mean, like, you know, today, the six plus two licenses that we announced.”

Wise is a unique opportunity with long-term compounding characteristics, as summarised by Founder and CEO Kristo Käärmann “So one thing to remind us is the investment horizon that we're investing behind is in is in years. So the things I talked about that we released today is not going to make the difference in numbers next quarter or even this financial year. But it's going to matter over the next decade. And and the investments over the next ten years will need the same long term focus, the same discipline to adhering to our principles financial model, because our shareholders own a company like no other. And in recent history, the one that has the foundations to eventually fix how money works across borders for people and for businesses.”

For more insights, see below notes:

2024.08.09 Wise 1Q25 Recap: Wise remains maniacally focused on the long-term opportunity

2024.10.16 2Q25 Trading Update Wise - reinvestment for sustainable growth