Wise - Investment Thesis

Wise is the disruptive leader, counter-positioned to win in cross-border payments

Investment Thesis

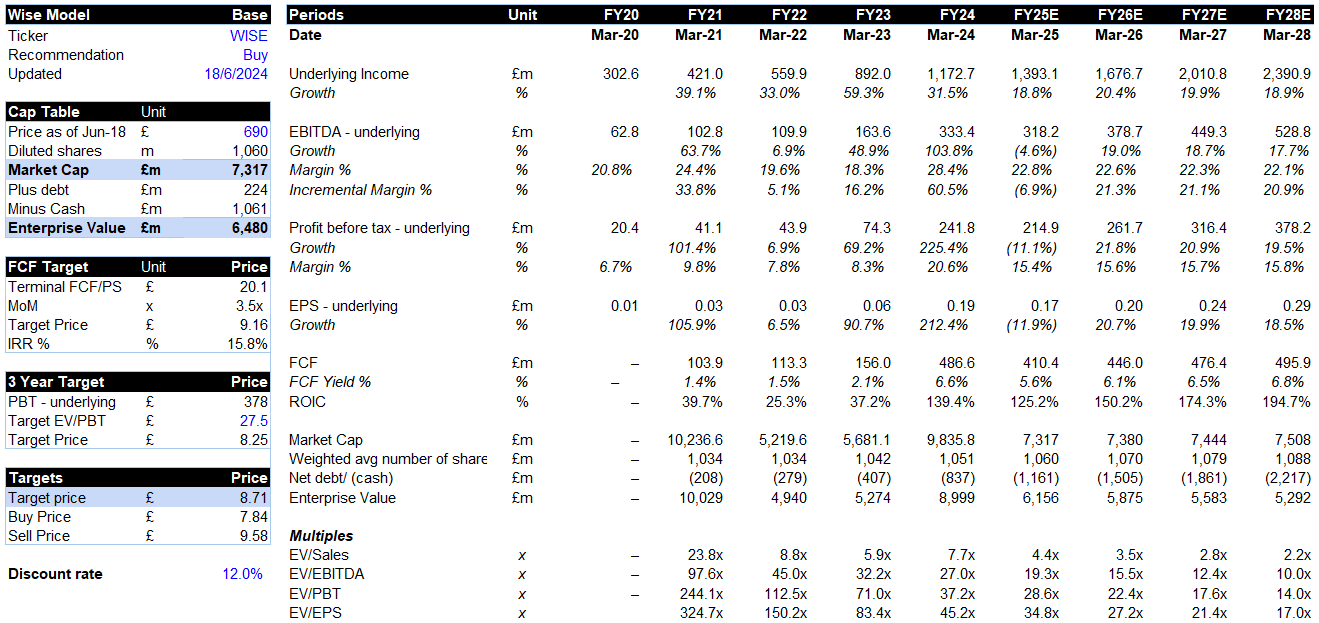

Wise is a high-quality business delivering the Amazon/ Costco playbook known as scaled economies shared in cross-border payments. Rather than realising scale efficiencies through higher margins, the near-term priorities are to drive long-term market share gains and outright leadership. This has seen margin forecasts return to mid-term levels, reflecting a reinvestment focus which is overshadowing the true earnings power of this business. Wise has free cash flow (FCF) conversion >90% and net cash levels above £800m. The current drawdown presents an attractive opportunity for long-term shareholders for the below reasons.

· Wise’s unique strategic approach and competitive advantages provides counter-positioning against incumbent legacy players (banks). The company consistently improves its value proposition as they share the benefits of scale with customers via lower prices, faster transfers and greater innovation. In contrast, legacy competitors have complex infrastructure and are structurally unable to lower take-rates and increase speeds to Wise’s levels. As Wise continues to build value, they can drive outsized market share gains and compound underlying income at 15%-20%.

· The company is founder led and has a long-term runway to be the dominant player in cross-border payments. The decision to reinvest and return underlying PBT margins of 20.6% to mid-term target levels of 13-16% reflects an internal mindset that prioritises durable competitive advantages over short-term profits. Wise has a significant opportunity ahead with market penetration <5% in Consumer while unit economics are remarkable reflected in ROIC of 139% and customer LTV/CAC of 16.4x. This validates the decision to reinvest.

· Wise is capital light and delivers substantial FCF from net interest income, providing business optionality and materially decreasing the future enterprise value. The company’s net cash position of £0.8b is expected to grow to over £2b by FY28 from high-margin interest income and strong FCF conversion. By incorporating net cash, Wise trades at an undemanding FY27 underlying EV/EBITDA of 12x and EV/PBT of 18x while growing underlying income at 20%. These metrics do not include benefits from interest income above 1%.

View: Accumulate – recent earnings and valuation re-base provide a solid entry point into a market leader with strong ROI and long earnings trajectory. Using a 50:50 blended discounted FCF and EV/PBT multiples valuation with a discount rate of 12% returns a target price of £8.71. Would be buying stock up to £7.84 at a 10% margin of safety to target price and an annual IRR of 15% over 4 years.

Company Overivew

· Wise is disrupting cross-border payments with a mission to facilitate “Money without borders – instant, convenient, transparent and eventually free”. The company is the lowest-cost provider, operating with scale advantages and a superior product proposition across its 160+ send currencies and 45 licenced countries. Wise has diversified beyond cross-border payments with revenue from interchange fees and interest income representing 22% and 10% of underlying income respectively.

· Wise is a founder led; customer-orientated business focused on delivering scaled economies shared. Near-term operating margins are being managed as the business returns scale benefits to deliver an increasingly superior customer proposition and competitive moat. The compounding aspect of Wise’s model means they will achieve outsized benefits in later years, through scale, margins, and competitive position. With time, this is a business that can generate significant operating leverage, with management understanding that payments is a scale game.

· Wise has strong operational momentum that is being overshadowed by negative market sentiment. Since 2021, Wise has accelerated active customer, revenue and earnings growth. While its multiple has contracted following a broad market sell-off of high growth businesses, margin disappointments and uncertainties around volume per customer (VPC). VPC has fallen due to lower high-value transactions, and a mix shift to card-only users who spend less but are stickier. Wise is a much better business now with significant FCF, a larger customer base, and more repeatable revenue.

Wise has a singular focus on disrupting a large industry dominated by banks known for opaque, slow, and expensive payments. The company is the leading FinTech by volumes and remains significantly underpenetrated, with current market share by volumes of <5% in the £2t Consumer market and <1% in the £9t Business (SME) market.

1. How durable is Wise’s Competitive Advantage

Wise differentiates through its purpose-built infrastructure and scale that brings speed, breadth of product and low prices. There are notable barriers to developing a truly global offering, with significant time and expertise required to establish global operations, support functions and regulatory licences across countries. We explore Wise’s competitive advantages further using Hamilton Helmer’s 7 powers:

1. Scale economies – Wise has scale and is delivering growth above competitors, which extends its leading position. The company has grown volumes from £42b in FY20 to £118b in FY24 representing a 30% CAGR. Compared to digital competitors, Wise’s volumes are 4x Remitly and 2.3x Payoneer. Scale brings greater operational efficiencies and enables Wise to sustainably lower prices and increase speeds. The company can also reinvest more in product development and geographical expansion. As noted, Wise will not generate scale efficiencies as it rebalances leverage back into growth investments.

2. Counter positioning – the industry is dominated by banks who have 66% share in Consumer and 90% in Business (SME) segments. They have high and opaque pricing, slow processing times, outdated technology, and subpar customer service. Banks are unlikely to adapt due to higher cost structures, domestic infrastructure, and the significant profits being generated from cross-border. These industry dynamics position Wise as the leading disruptor to take share over a long duration.

3. Process Power – Wise has unique IP by owning the infrastructure stack, with 65+ regulatory licences across 45 countries, and 5 direct connections to real-time payment networks. This network scale is difficult to replicate, and provides the company with seamless access to data, and control over the end-to-end payment process. Wise can also drive continuous improvements across speed (62% instant transfers), cost, and risk management while competitors have chosen not to own large parts of the infrastructure.

4. Brand – Wise has a trusted brand, with a 60+ NPS and a 4.3-star Trustpilot rating. The company has cultivated strong brand equity by prioritising customers, including an initiative to return interest income through cashbacks and interest products. The industry dynamic and Wise’s strategic approach means they will not leverage brand to raise prices.

5. Network economies – 66% of new customer acquisition comes through word of mouth, delivering a network effect as the customer base grows. An increase in users also makes the platform more efficient as it improves the ability to net currencies and increases the capacity to spend on R&D.

6. Cornered Resource – the culture at Wise and small, autonomous teams drives high-performance outcomes and enables the business to grow quickly while delivering innovation.

7. Switching costs – industry has low switching costs due to the fragmented competitive landscape and minimal fees and time required to change platforms. The company has improved customer repeatability and loyalty by introducing new products such as its multi-currency account, where users are transacting 3x more.

Wise has clear competitive advantages such as scale economies, counter-positioning and process power that differentiates the company in the fragmented cross-border payments industry. The group’s scale and reinvestment focus will make it increasingly difficult for competitors to follow as the strategic flywheel enhances the value proposition further. These competitive advantages will improve with time and scale.

2. What happens to take-rates

Wise has shown consistent price leadership by lowering cross-currency take-rates as its cost to serve declines. Online comparisons generally show Wise as the cheapest option, especially for transactions greater than US$10,000. Table 1 below compares the company’s take-rates, cost to serve and margin differential with listed competitors. As Wise’s cost to serve falls due to scale efficiencies, they can sustainably lower prices while maintaining cross-currency gross margins. In contrast, competitors have a structurally higher cost to serve or take-rate and should experience margin pressures.

Despite lowering cross-currency take-rates, Wise can still manage to grow overall take-rates due to rising Other fees from card interchange, domestic transactions, and new products. Graph 1 below shows my forecasts for a rising take-rate, which is above consensus expectations primarily due to Other Fees.

3. Can Wise compete against Visa and Mastercard?

Visa and Mastercard are formidable competitors with robust infrastructure streamlining cross-border payments. Visa, via B2B Connect, Visa Direct, and CurrencyCloud, facilitates cross-currency capabilities for over 500 payment organisations, including Stripe, Adyen, Revolut, Etoro, Remitly, Moneygram, and more. These organisations harness Visa's speed, efficiency, and transparency by connecting to 36 Automated Clearing House (ACH), 12 Real-Time Payment (RTP), and 15 card networks spanning over 7b endpoints. Mastercard Send also collaborates with banks and other entities to modernise cross-border services.

Partnering with Visa means these organisations have instant access to leading infrastructure. Wise also uses these services where it makes sense but chooses to own most of the infrastructure. For those completely partnering, they are reliant on external service providers and have a fixed cost per transaction. Rather, Wise benefits from efficient data flow, the ability to lower costs and fewer middlemen.

Visa and Mastercard also compete directly with Wise Platform. These players have great infrastructure but lack the overall product proposition and global support. Wise has a broader solution that provides access to its payment rails, regulatory expertise, range of products and global support and operations. Given the size of the opportunity, multiple players can win. Domestic banks may find Wise appealing due to its multi-currency accounts and comprehensive compliance, AML, and fraud management. Others may opt to outsource just only the payment rails, which Visa and Mastercard can provide.

4. Can Wise continue to grow active customers above 20%?

Since FY20, Wise has grown active customers at a 29% CAGR to 12.8m, with word of mouth representing 66% of new adds. As its customer base increases, this network effect grows. In addition, Wise Platform, the full-stack solution for partners such as legacy banks, neobanks, and SaaS companies adds another lever for growth. The solution is a highly effective channel to acquire customers at low cost and scale, with 85+ partners signed to date.

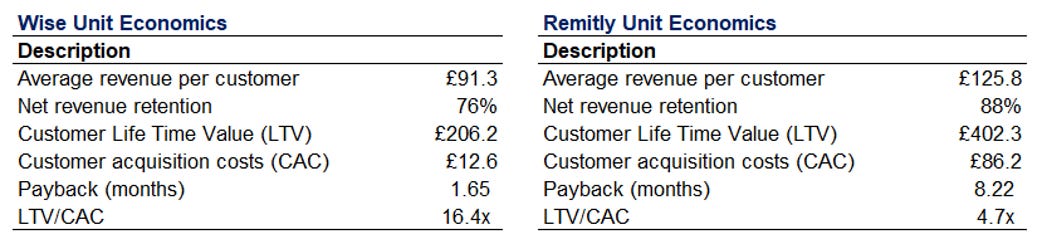

Wise also has the capacity to reinvest more into sales & marketing (S&M), which trends around 5.1x and 4.2x lower than Remitly and Payoneer. Its unit economics are currently very strong with an <2 month payback period and >16x LTV/CAC, well above the 3x LTV/CAC that is considered leading. We compare the unit economics of Wise and Remitly below.

The company’s decision to spend more is validated by these metrics suggesting they will achieve positive returns on investment. The result is that Wise should continue to capture market share gains and accelerate active customer growth with my forecasts implying a 22.6% CAGR to FY28.

Valuation

Wise trades on an underlying forward EV/Earnings of 35x and EV/EBITDA of 19x, with limited capitalisation. Note, FY25 considers a rebasing of earnings as Wise reinvests for long-term growth. My estimates from FY25 have underlying revenue and profit before tax growth 3-year CAGR of 20% and 21% respectively.

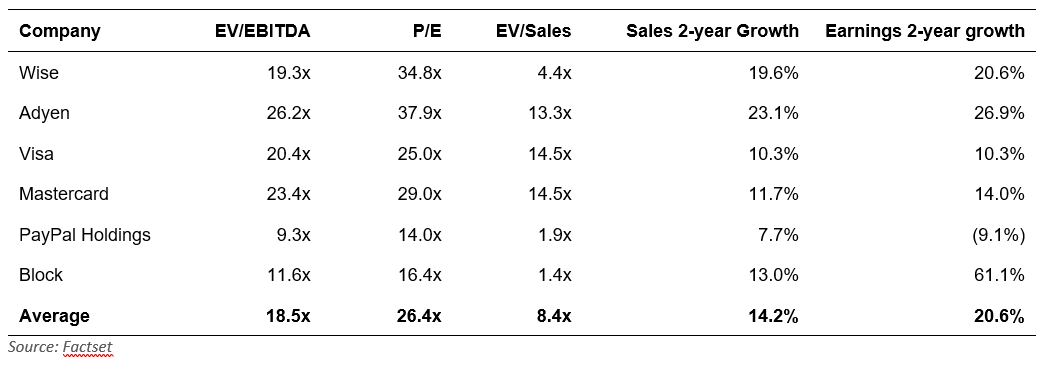

Wise trades favourably compared to historical multiples due to multiple contraction and an uplift in earnings and free cash flow. The below table compares the valuation of global payments peers with Wise.

Visa and Mastercard trade on forward P/E multiples of 25x and 29x respectively, growing earnings at low to mid-teens. Although its competitive moat is less established, Wise deserves a premium due to its faster growth, significant near-term free cash flow conversion, notable reinvestment, greater runway and margin upside. If we include interest income, Wise trades on an EV/earnings of 20x which implies a discount to these networks. Adyen is a more comparable business with similar long-term growth prospects, trading at 38x forward P/E.

Compared to industry peers, Wise trades at a premium. Note, these are statutory instead of underlying figures, which includes interest income and is more comparable to peers. The valuation premium is warranted considering Wise’s growth prospects and leadership position. Peers are delivering lower quality growth.

Longer-term metrics are more compelling with Wise trading on a FY27 underlying EV/EBITDA of 12x and EV/EPS of 21x, with earnings growing at 20%.

Risks

Risks to the investment thesis include:

· Increased losses from foreign exchange volatility and financial crime. Wise has reduced these risks by netting transactions and using its machine learning based treasury system to detect events and predict liquidity needs. If these losses increase, earnings come under pressure and customer trust would decline.

· Competition is able to improve its value proposition and scale faster than Wise. Wise faces competitive threats from existing FinTech’s including Revolut through CurrencyCloud. There are also emerging technologies such as interlinked domestic payment systems, major payment networks like Visa, and even social media platforms. If these competitive threats strengthen, churn should increase and growth slow. Wise is developing a solution that is faster, cheaper, and more convenient and is proactively investing to deliver what these new technologies eventually aim to bring.

· Reputational loss. The company runs the risk of expanding too quickly and for issues to occur. Wise has experienced outages and operational issues. Recently, they paused the onboarding of new business customers in 13 European countries to upgrade the servicing and operational capacity within the region. If Wise grows unsustainably, it can impact customer satisfaction and firm reputation. Wise understands these risks and has responded by developing robust cloud-native systems with automation, while taking a measured approach to expanding and building a sustainable business.

Disclaimer: All posts on “cosmiccapital” are for informational purposes only. This is NOT a recommendation to buy or sell securities discussed. Please do your own work before investing your money.