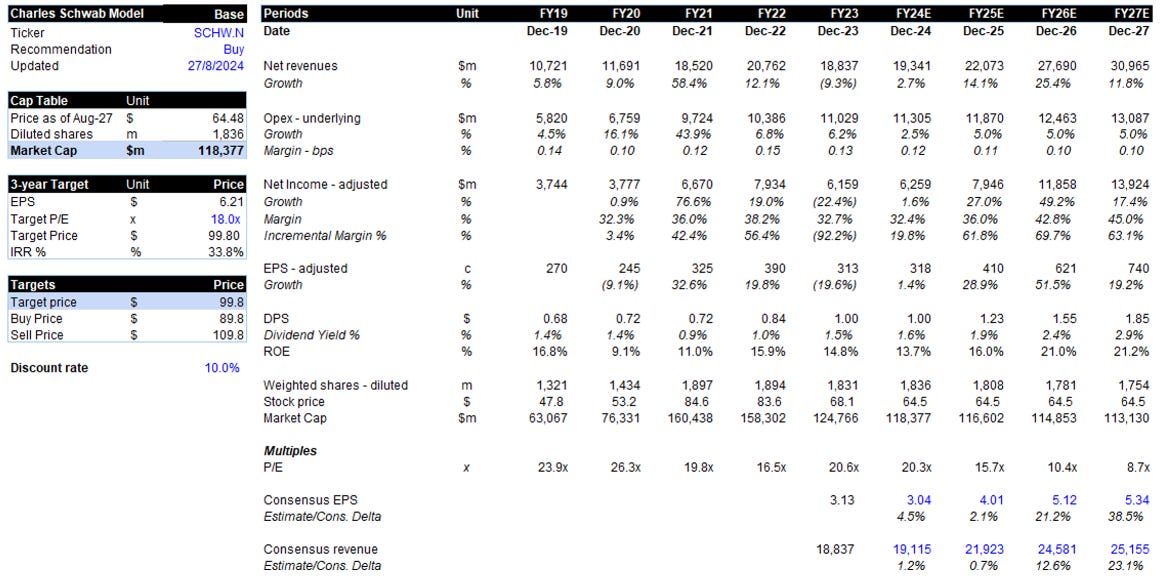

Charles Schwab - Investment Thesis

The current environment presents the optimal backdrop for Charles Schwab

Investment Thesis

Charles Schwab is a leading provider of financial products and solutions for investors and advisors, holding 14% share of US retail assets. The company leverages its scale and structurally lower cost base to consistently deliver value for customers. Schwab is now in an enviable position where its balance sheet and earnings are both inflecting in the right direction. See below.

1. Customer cash realignment shifts from a headwind to a tailwind. The significant increase in interest rates from near-zero to over 5% in 2022 led customers to transition cash into money market funds, where Schwab does not earn interest income. This saw interest earning assets (cash) fall from 9% to 4% (historic lows), while consensus has this falling further to 3%. Historically, changes in interest rate often have an inverse relationship with customer cash levels as seen in the graphs below. However, consensus estimates suggest a continued reduction in customer cash as interest rates decline.

There are also a multitude of other factors such as the completion of the TD Ameritrade acquisition and seasonally higher cash outflows in the June quarter, which reinforces the view that cash realignment is likely behind Schwab. My estimates indicate a gradual improvement in customer cash levels as the company returns to higher net new asset growth and benefits from interest rate cuts. The result would see significant incremental profits above consensus estimates.

2. Schwab’s balance sheet improves materially while net interest margins (NIMs) rise from 2% to 3% by FY26. As interest rates rose and customer cash balances fell, the group relied on expensive short-term funding to cover outflows, while a substantial portion of its assets (4-year duration) remained locked in at lower long-term rates. As a result, NIM expansion was only modest.

With cash realignment easing and most of the TD integration behind them, the business can quickly pay down this costly debt and gradually reinvest expiring assets into higher-yielding securities. The mix-shift is illustrated below.

An increase in higher-yielding assets coupled with a reduction in higher-yielding liabilities allows NIMs to sustainably expand to 3%. This results in incremental net margins above 55% from FY25 while ROE rises to 20%.

3. The merger with TD Ameritrade consolidates Schwab’s closest competitor and creates a financial services leader with almost $10t of client assets and 14% market share. The transaction reduces competition at the top level, with Fidelity the only other viable platform operating at scale. Further, with the TD integration now complete, Schwab can refocus on the core business with scope to improve monetisation and drive synergies.

View – Accumulate, Schwab is a high-quality business with leading financials, significant market share, profitable growth and improving returns on equity. Following a period of subdued profits and elevated capital requirements, Schwab is poised to deliver EPS constant annual growth rate (CAGR) of 27% to FY26. Applying a 18x multiple on FY26 EPS of $6.21 and discounting this back returns a target price of $99.8, representing 55% upside to today’s share price. Would be buying the stock up to $90, which is a 10% discount to target price.

Market and Variant view

Factset estimates have 3-year revenue CAGR of 9% and EPS of 18%, reflecting robust growth in trading and net interest revenue and improving margins. The sell-side is broadly positive with 65% of analysts having buy ratings. If Schwab achieves consensus forecasts of 18% earnings growth, the stock is likely to re-rate. The variant perception is for interest earning assets to rebound as explained above.

Company Overview

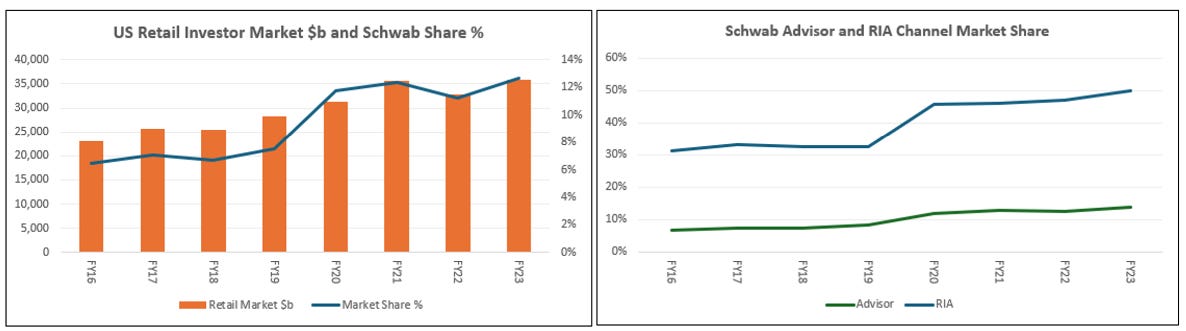

Schwab is a leading US financial services provider of brokerage, banking and advisory services. Over the past 50 years, the business has evolved from a discount broker into a provider of low-cost services across a broad selection of financial products for retail and advised assets in the US. Schwab has scale economies and consistently reinvests these benefits back into product, technology and prices to deliver better value, service, transparency and trust. They have seen improving and high levels of customer satisfaction with NPS scores across segments ranging from 60-80.

As a founder-led business, Schwab prioritises customer-first outcomes and long-term competitive advantages. This is best illustrated in its decision to cut trading commissions to zero in 2019 disrupting itself and the industry by impacting short-term profits and stock prices. Schwab then opportunistically acquired its nearest competitor TD Ameritrade at a discounted valuation, growing market share from 8% to 13% and consolidating two leading platforms.

Schwab operates primarily through two segments, Investor and Advisory services. Investor Services offers retail investors a virtually free platform to invest across most asset classes. Advisory Services provides low-cost advisory, tax and custody services for Registered Investment Advisors (RIA). Schwab’s platform has reduced the barriers and been a core driver for advisors seeking independence from traditional Wirehouses and broker-dealers such as Morgan Stanley to the RIA model.

Revenue is derived from four main sources:

1. Net interest (50%) – interest spread on uninvested customer cash balances

2. Asset Management (25%) – fees on Schwab owned mutual funds and ETFs and fee-based advisory services

3. Trading (17%) – commissions on options, futures and third-party mutual funds and order flow.

4. Other (8%) – bank deposit account fees where uninvested cash is swept to TD Bank

The revenue mix has shifted from Trading contributing 50% of revenue to interest income being the largest component today.

Is Charles Schwab a quality business?

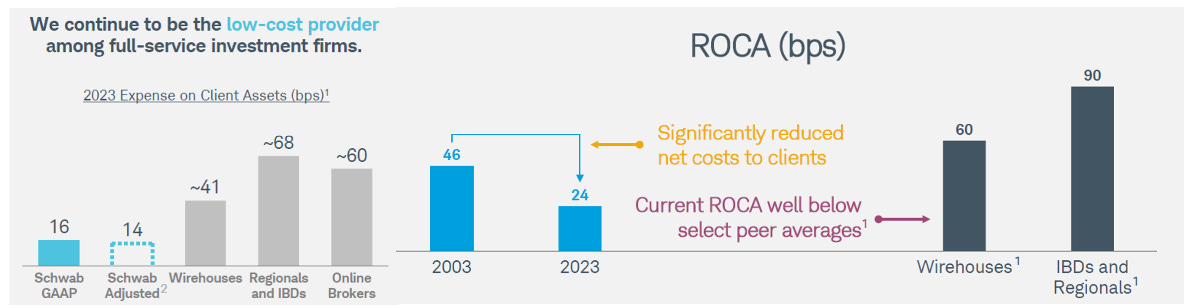

While Schwab operates in an industry with moderate switching costs, it has developed sustainable competitive advantages through scale, IP and brand. The main enabler of this is a structurally lower cost to serve, allowing Schwab to return material benefits to customers in the form of lower revenue on client assets (ROCA), which sits 2.5x lower than Wirehouses and other competitors. Schwab has continually reinvested back into its value proposition, which includes zero fees on custody fees and trading commissions. As they continue to reinvest in this flywheel, competitors are increasingly unable to match them as they operate with a structurally higher cost base.

The low ROCA also implies Schwab is likely under earning and has the opportunity to extract more revenue by providing value. Despite being the low-cost leader, the company still generates impressive pre-tax margins of 41.5%.

Schwab’s customer-first approach has fostered a trusted brand and cultivated sticky relationships which is core to increasing net core assets by 5-7% per annum. There are really only two reputable brands in Schwab and Fidelity operating at scale and a comparable value proposition that investors trust with large sums of assets. With this backdrop Schwab is a business with sustainable competitive advantages and a long runway to gain share.

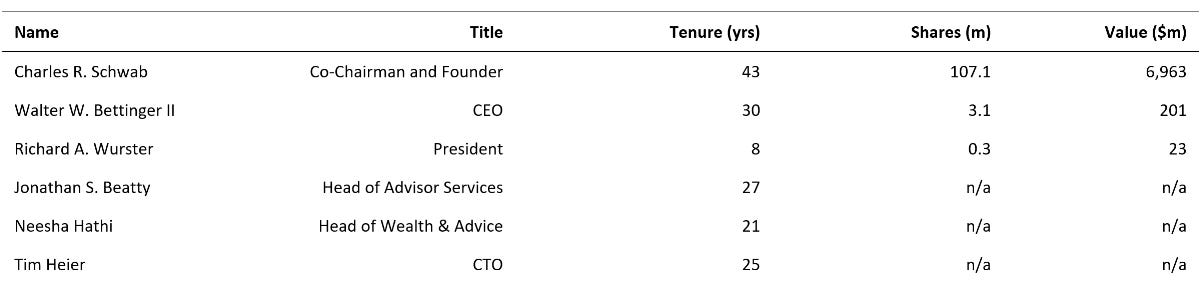

Management and Positioning

The key shareholders are TD Bank 9.9%, Charles Schwab (founder) 6.0%, Vanguard 6.8% and BlackRock 5.4%. Other internal directors and management own 6.6% equity. Incentives are heavily weighted to variable pay (89%) with targets centred around diluted EPS and return on tangible capital employed. Recently, there has been management turnover, with the COO, CFO and Head of Advisory Services either retiring or transitioning to the Board/ Advisor roles. Importantly, these changes were announced after the completion of the TD integration, while replacements are mostly internal hires reflecting the solid culture. Management ownership and tenure is shown below.

Valuation

Charles Schwab trades on a forward P/E of 18x, which is below its 10-year historical average of 20x. The company is a premium to banks on 10-14x forward P/E, and other wealth management firms such as Raymond James on 12x P/E. The multiple is reasonable given Schwab’s leadership qualities, sustainable market share gains, scalable model and 20%+ earnings growth.

Risks to view

The counter view is for interest earning assets to materially decline while increased competition and a difficult TD integration could see elevated churn.

· Interest rates – continued rise in interest rates may see cash balances fall further. Customer cash is already at historic lows, with the more likely scenario being a shift in asset allocation. Also, higher rates would likely see NIM expansion, offsetting some cash downside.

· Regulation – seen increased scrutiny around capital levels which has increased costs. There is also pressure from the SEC on banks such as JP Morgan and Wells Fargo regarding cash sweeping practices. Schwab should be less impacted as they have encouraged clients to realign cash by providing multiple options for higher-interest securities.

· Outages and brand damage – customer trust can diminish quickly with outages and issues across the trading platform. As switching costs are low, we could see elevated churn and lower growth in net assets. This is something to watch with Schwab having seen issues since the TD Ameritrade acquisition.

· Competition – more prevalent in the retail trading space where digitally native platforms such as Interactive Brokers and Robinhood compete. These players are capital light, and in the case of Robinhood have spent aggressively to acquire customers via cashback offers. While ones to watch, they target a smaller portion of Schwab’s customer base, and do not have meaningful scale and trust to attract larger asset holders.