Synopsys - Investment Thesis

Synopsys is enabling the proliferation of chips but with minimal margin of safety

Investment Thesis

Synopsys is the leading provider of mission-critical electronic design automation (EDA) software and IP components driving the proliferation of chips and systems. Its solutions are critical for the likes of chips (Nvidia) and systems (Amazon) companies as they develop advanced chip designs. Synopsys operates in a highly attractive industry that does not have the typical semiconductor cyclicality with its revenue influenced by R&D budgets rather than semiconductor revenue which is lumpy. The market therefore has durable characteristics and its duopoly-like structure alongside Cadence Design is highly attractive. Synopsys is the preferred market exposure for the below reasons.

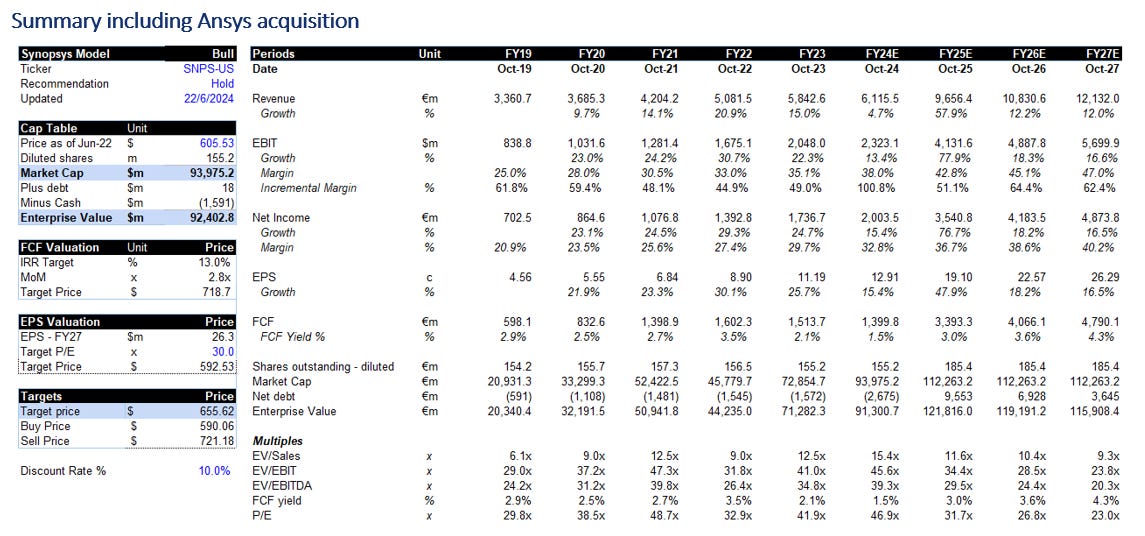

1. Synopsys will become a more focused business with a higher margin profile, through its divestment of Software Integrity (15% EBIT margins) and acquisition of Ansys (53% EBIT margins). Operating margins grow from 35% in FY23 to 43% (including Ansys) in FY25. The transactions also create a more aligned business model with clear focus on driving more efficient outcomes from chips to systems.

2. The company is the leader in Digital EDA and number 2 in IP, providing scale benefits within two segments growing faster than the overall EDA market. This exposure also drives operational synergies and diversification benefits. Cadence has lower exposure to IP, representing 12% of revenue and remains one-third the size of Synopsys’.

3. The Ansys acquisition delivers both financial and strategic value for Synopsys. Financially, Ansys brings $800m of near-term cost and revenue synergies and $1b of longer-term revenue synergies. The transaction also expands the Total Addressable Market (TAM) by $10b to $31b. Ansys' leadership in simulation and analysis strategically complements Synopsys’ existing design solutions, creating an integrated ecosystem for systems companies to drive more efficient chips to silicon. Synopsys would be better positioned to compete against Cadence, who currently have a solid solution in this space.

Synopsys is a high-quality business with durable competitive advantages, a solid management team and incremental margins above 45%. Financially, the business can deliver mid-teens earnings growth with high visibility due to 81% recurring revenues.

View – Hold, while business fundamentals are strong, there are near-term risks around the regulatory approval for Ansys and geopolitical tensions with China, which represents 15% of revenue. Synopsys trades at forward P/E of 42x, reflecting a 53% premium to 10-year historical averages and 46% premium to the NASDAQ.

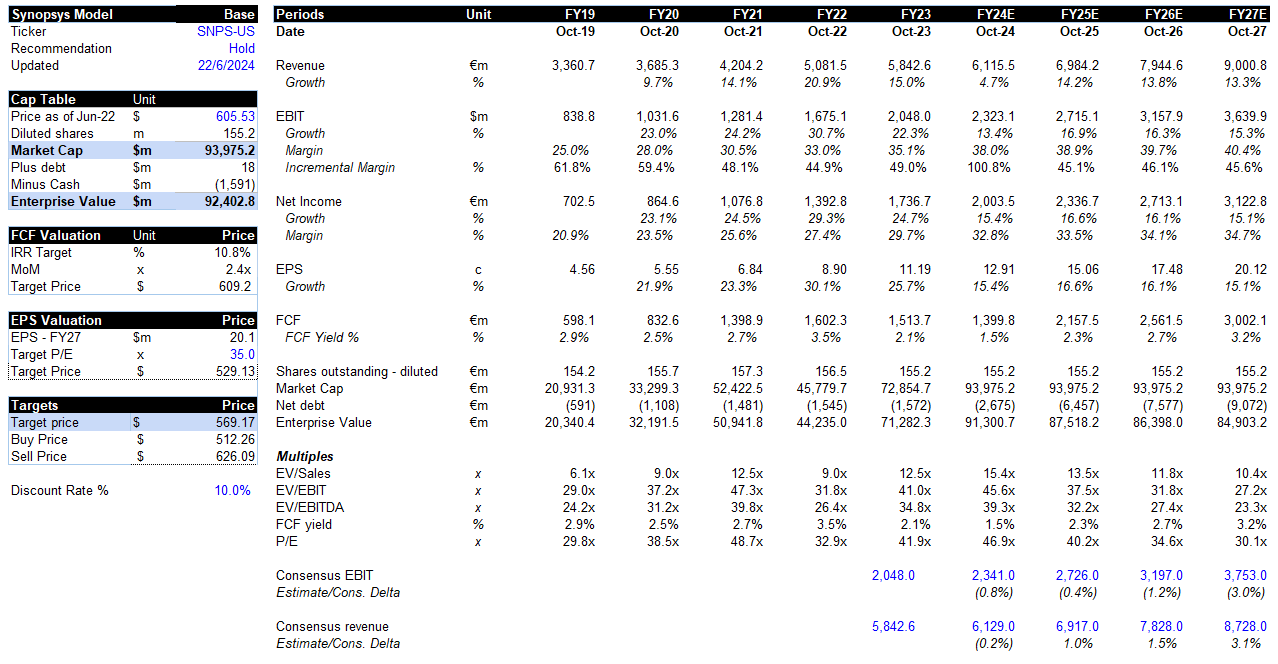

Excluding Ansys, a blended 50:50 discounted FCF and P/E multiple valuation returns a target price of $569. Note, there is upside if Ansys get approved, with the blended valuation increasing to $655. Would prefer buying Synopsys at $512 which implies a 10% discount to the target price excluding Ansys.

Market and Variant view

Factset estimates have 4-year revenue growth compound annual growth rate (CAGR) of 11% and EPS growth of 16.3%, taking into consideration the divestment of Software Integrity but not Ansys. The sell-side is positive with 19/24 analysts either a strong buy or a buy. My estimates for FY24 are slightly below EBIT consensus levels. Including the Ansys transaction and synergies, Synopsys would trade on a FY25 P/E of 31x vs current P/E of 42x. Could get a good opportunity to buy this if the share price remains stable following the approval of Ansys.

Company and Industry Overview

Synopsys has two operating segments. Software Integrity is being divested this year.

1. Design Automation (65% revenue) – EDA software for the design and verification of chips

2. Design IP (25% revenue) – known as silicon proven IP which is a reusable unit or building block being licenced for use in chip designs

3. Software Integrity (10% revenue) – application software to test the quality and security of code

EDA is mission-critical for companies developing smaller and more complex chips. Without them, the technological advances seen at the likes of Nvidia would not be possible. Market growth has accelerated from mid-single digit CAGR (circa 5%) in FY18 to 12% in FY23 due to semiconductor industry growth and increased design starts from systems companies who are choosing to customise their own chips. Synopsys expects the EDA market to continue compounding at 12% over the next 5 years.

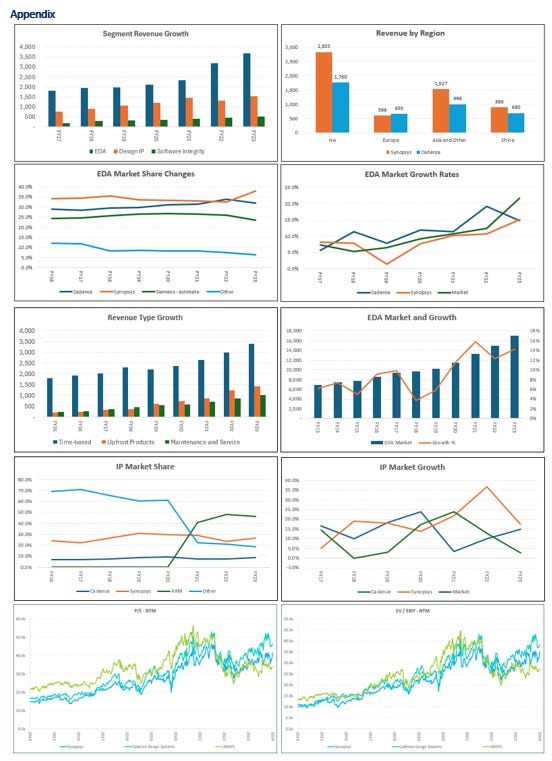

The industry is effectively a duopoly consisting of Synopsys and Cadence, and to a lesser extent Mentor (now owned by Siemens) who caters for a niche. Synopsys has leadership in Digital Design & Verification with its share estimated at 70%. These are the more advanced chips that are driving the next industrial revolution. Cadence is the outright market leader within Custom Design referred to as Analog, with its share estimated to be 90%. Competition is fierce, with product bundling and technological advances often key to gaining share. Cadence has grown its share in Digital and Verification through its ARM partnership. As per the Appendix, Synopsys has regained share losses since 2022 with the overall split currently Synopsys 38% vs Cadence 32%.

In IP, Synopsys is the outright market leader in Interface & Foundational IP with around 42% share. The company has a small presence in Processor & Other IP, with ARM the dominant player. Synopsys has grown its overall share in IP from 13% in 2015 to 22% in 2023. The industry has delivered 12% CAGR with the key trend being the increased outsourcing of IP as customers focus skilled resources on differentiating aspects within the chips.

1. How Durable is Synopsys’ Competitive Position?

Synopsys and Cadence are the two dominant industry players with a full suite of EDA and IP solutions. Synopsys has sustainable competitive advantages which we explore further using Hamilton Helmer’s 7 powers:

1. Process Power – the hallmark of this business. Consistent product iterations since founding 28 years ago has developed a portfolio of solutions that is very difficult to replicate due to the size and duration of reinvestment along with the close working relationships with leading semi players driving global innovation. Synopsys is leading in Digital design and Verification, while Cadence is more advanced in Analog.

2. Scale economies – the company has leading market positions and has leveraged this scale to reinvest more in R&D (33% of revenue) and S&M (15% of revenue). This makes the barriers very high for new entrants to bring comparable products to market as the investment required is significant. While reinvestment levels are elevated, Synopsys has also been able to deliver incremental margins above 45% and group operating margins of 35%. In IP, scale is evident through 8k unique titles, 6k R&D engineers, and deep customer relationships across 30 foundries.

3. Switching costs – these are moderate to high as EDA is mission-critical and switching does cause disruption. Although, most chip design firms will have a combination of both Cadence and Synopsys products, which has seen tools being interchanged across the top two players. Customers primarily switch between products as they start new designs; the reasons being due to price, quality or greater buying power. Bundling has often been used to gain share, with weaker products sometimes included in a package for free. As EDA technology becomes more complex, we could see less switching. In IP, switching costs are moderate as a new vendor would just need to build a relationship and develop a product that fits the customer’s needs.

4. Brand – well-known brand with strong reputation. Due to competition, semi-industry cost pressures and buying power of customers, the company has not really leveraged brand to deliver pricing improvements. There is latent untapped pricing power, which can be realised over time as customers increasingly recognise EDA as a technology differentiator rather than a cost centre.

5. Counter positioning – Synopsys is the market leader and the incumbent. It is unlikely a new player can come through with a superior business model due to the company’s scale of reinvestment, strong brand and existing relationships with leading semi companies.

6. Network economies – not really a network effect business. Although, technology is fast-paced and products will often become a competitive disadvantage if a customer does not adopt it.

7. Cornered Resource – 28 years of reinvestment and innovation. EDA is developed from cumulative knowledge and constant iteration to get to the current state. This is very difficult to replicate without going through this same iterative process over a long duration. We have seen Chinese competitors with significant funding struggle to make an impact.

2. Can the EDA and IP industry sustain double-digit growth rates?

The EDA industry’s 5-year CAGR has accelerated from 5% in 2018 to 12% in 2023 driven by:

Traditional semi customer growth – 8%

R&D budgets up 7% annually

EDA software taking a larger portion of R&D spend, having grown from 13.6% to 15%

Increased take-up of products ie Verification, complex chips requiring more of this and being done earlier in process

Cadence’s verification revenue has grown at a 17% 5-year CAGR

New products across AI and systems simulation

New Systems customers outside of the traditional semiconductor industry – 4%

Systems companies represent 45% of revenue at Cadence and Synopsys

Includes hyperscalers, EVs and aerospace players

Amazon began designing chips in 2014 and continues to expand this capability.

Graviton chips provide 40% better price-performance than leading x86 processors

Graviton 4 has 30% better compute performance and 75% more memory bandwidth than Graviton 3

Synopsys expects the EDA market to continue growing at 12% 5-year CAGR, driven by secular trends above including chip designer talent constraints, rise of software-defined systems, and increased chip complexity (smaller and stacked). Growth will come from a combination of more users, products and customers. The growth runway within system companies remains nascent and the benefits Amazon has seen suggests penetration will continue to grow. The industry double-digit estimates therefore seem reasonable.

IP industry 5-year CAGR was 12% both in 2018 and in 2023 driven by:

Design starts growing at 6%

Greater outsourcing of IP from semiconductor players ∼30% remains in-house

New customers and faster tech cycles – systems companies

Silicon proliferation and AI – increasing number of chips

Complexity of chips – multi-die requires more IP

Synopsys forecasts the 5-year CAGR to be 15%. The multiple drivers of growth for IP above EDA enables it to grow faster.

3. Can Synopsys win against Cadence?

Competition among Synopsys and Cadence is strong. Both players have a full-suite of products that have been seen as homogenous and interchangeable. Customers will often use a combination of software across both providers, driving innovation and bringing greater buying power during contract renegotiations.

Since FY18, Cadence has gained share in Digital & Verification through its ARM partnership and continues to remain a material threat. The company has a strong portfolio in System Design and Analysis, competing against Ansys and having grown faster. Synopsys has regained EDA share losses in recent years and my expectations have them maintaining share in this growing market based on:

An improved offering with new innovations such as its integrated Fusion platform and AI products

Leadership position in Digital exposes it to a faster growing segment driving advanced chip development

Leading AI products – full-suite of AI products driving improved automation, data analytics, generative AI benefits. The company is leading in AI, with its products all being released ahead of Cadence. AI should be a key differentiator and can drive better pricing outcomes in the future.

Ansys strengthens Synopsys’ capabilities in advanced chip design for systems companies and expands the TAM.

Within IP, Synopsys is highly differentiated through scale economies. The company is seen as a trusted and proven partner, with a broad portfolio of highly differentiated IP and close working relationships with multiple foundries. For these reasons, Synopsys will continue to gain share and win against Cadence here.

Management and Positioning

The key shareholders are index and large mutual funds including Vanguard, Blackrock, and Capital World Investors. The management team has been refreshed since 2021, see below. Culture is solid and performance driven, underpinned by the incentive structure; CEO remuneration is 88% variable-based with targets around operating margins, revenue growth and relative TSR.

Valuation

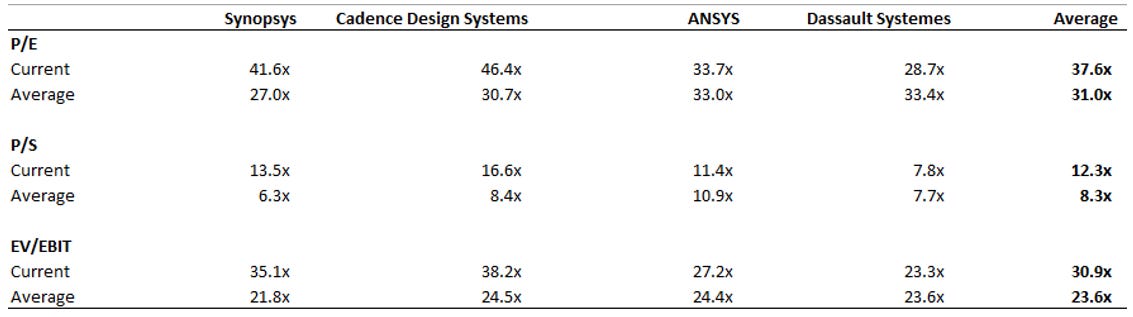

Synopsys trades on 42x forward P/E, well above its 10-year average of 27x. Multiple expansion since 2019 is attributed to higher industry growth, an improved market position and significant margin expansion; operating margins have grown from 24% in FY17 to 35% in FY23. The company trades at a discount to Cadence at 46x forward P/E with its nearest competitor having experienced solid growth and a higher margin profile. While Synopsys’ market premium is warranted, the absolute figures are unfavourable compared to other high-quality businesses such as Microsoft (32x), Alphabet (22x), TSMC (20x) and ASML (40x).

Risks to view

The counter view is Synopsys has benefited from unsustainable industry growth which should revert back to normalised levels. Valuations should also de-rate. In addition, Cadence could see market share gains, especially in Digital & Verification where Synopsys is the leader.

Ansys – the risk is the acquisition falls through or is poorly integrated if it does. Synopsys would be strategically disadvantaged if this happens as Cadence currently has a stronger simulation and analysis offering. A general comment is that large acquisitions generally take longer than expected and do not end well. Although Ansys and Synopsys have a 7 year partnership developing products and bringing the two cultures together which de-risks this.

Market share losses – Cadence grows faster by either winning deals through bundling or differentiating its products. This has occurred at times historically. Synopsys is well positioned now having reinvested significantly to deliver more innovation through AI and a platform of products.

China – we could see further restrictions on trading between the China and Western countries. This could cause headwinds to industry growth. In addition, 15% of Synopsys’ revenue comes from China, which has grown faster than group levels since 2020. This growth is questionable given China’s investments towards building a domestic semiconductor industry and self-sufficiency with lower reliance on Western counterparts like Synopsys.

Industry design starts decline due to industry consolidation or as systems companies return to outsourcing. Industry consolidation has generally been a headwind for EDA software due to lower overall design starts and R&D team optimisation. Also, as discussed systems companies have started to design their own chips, which could become a headwind if they revert back to relying on outsourced chip designers such as AMD, Intel and Nvidia. Insights from Amazon suggest otherwise due to the significant technological efficiencies and cost savings they get.