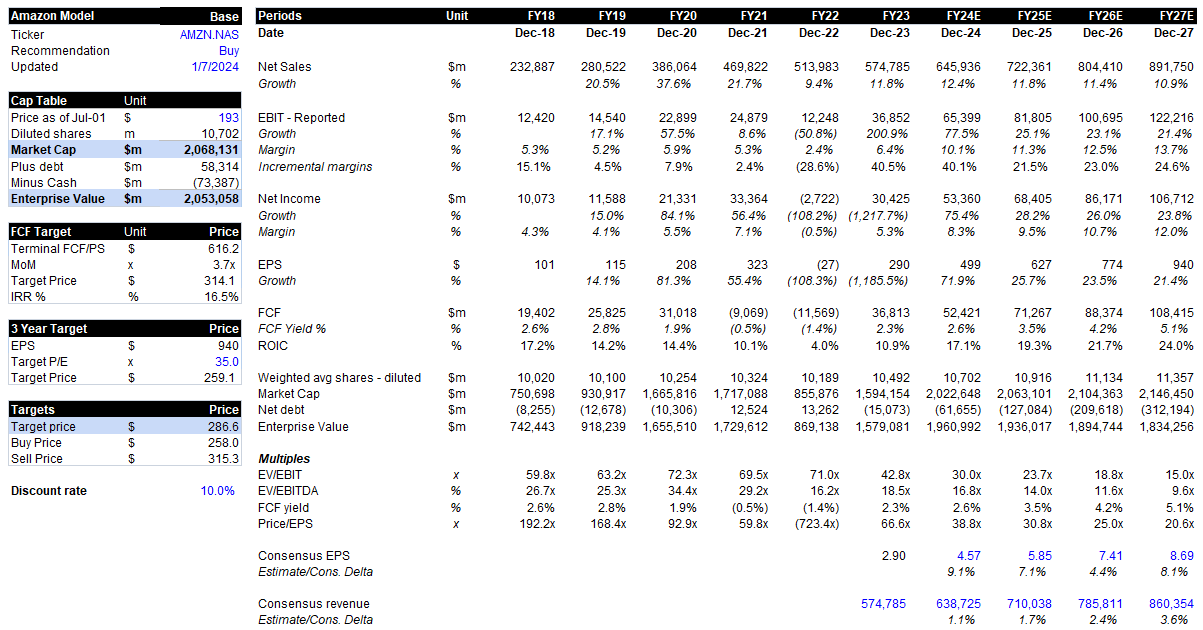

Amazon - Investment Thesis

Amazon is at an operational and financial inflection point

Investment Thesis

Amazon has carved out the number one positions in Ecommerce and Cloud Infrastructure. While the company enjoys significant scale advantages, this is not yet reflected in its margin profile. Rather, long-term reinvestment has delayed operating leverage in favour of returning scale efficiencies to stakeholders through lower prices, faster delivery, greater selection and broader benefits via Prime membership. While still a clear priority, Amazon’s mix-shift and cost optimisations see incremental EBIT margins inflect from FY23 and beyond. Amazon represents a compelling opportunity to invest in a growing leader that has both operational and financial momentum.

1. Amazon has clear competitive advantages in Ecommerce that continues to drive share gains. Its superior value proposition is underpinned by scaled infrastructure, a significant network of buyers and sellers and extensive customer benefits through Prime. Further, the customer-first obsession drives continuous improvement and reflects a competitive proposition that makes it very difficult for new or existing entrants. Amazon is the clear Ecommerce leader, and there is no pure-play platform in its markets operating with the same level focus and scale across technology and infrastructure.

2. Amazon operates in highly attractive markets with notable long-term growth runways. In Ecommerce, adoption in the US sits at 22% of adjusted retail sales, while penetration is lower across most International markets. China provides a barometer for longer-term penetration, with Ecommerce representing 46% of sales. For cloud, the market was created in 2006 and only represents 15% of total IT infrastructure spend. This dynamic is expected to flip, as cloud infrastructure becomes 85% of the market, increasing 5-6 fold from current levels. Amazon is well positioned as the leading player in both these segments.

3. The mix shift to higher margin Advertising, AWS and Third-party Seller revenue delivers material operating leverage. These faster-growing segments bring a meaningful change in Amazon’s margin profile, with incremental margins above 20% vs mid-single digit levels historically. These margin improvements do not reflect material upside from retail margins, which continues to under earn compared to traditional retailers.

View – Accumulate, opportunity to own the highest quality Ecommerce business and leading cloud player with sustainable industry dynamics and improving ROIC and margins. The company trades at a forward P/E of 37x, growing earnings at a 34% 4-year CAGR. Using a blended 50:50 discounted FCF and P/E multiple valuation returns a target price of $286, 48% above current share price. Would look to purchase Amazon up to $258, representing a 10% discount to target price.

Market and Variant view

Factset estimates have 4-year revenue CAGR of 11% and EPS of 32%. The sell-side is positive with 63/66 analysts either a strong buy or a buy. My revenue and earnings estimates are 2% and 7% respectively above consensus, highlighting the margin upside potential from the revenue mix-shift. Further, if Amazon can show the sustainability of its long-term earnings growth, the market will begin to appreciate this by maintaining or expanding this multiple.

Company Overview

Amazon is a highly innovative, technology led business that is disrupting the traditional way of doing things. The company began as one of the first to market in Ecommerce, originally selling books and then expanding into everything retail. Amazon has continued to iterate and disrupt itself with new offerings including Prime membership, third-party sellers, devices such as Echo and Kindle. The innovation reflects a company culture that prioritises long-term thinking and an owner’s mindset. The Ecommerce value proposition has been developed in the US and is being replicated Internationally across 21 additional countries.

Amazon launched AWS in 2006, an initiative to on-sell excess data centre storage and compute to other organisations. The company essentially created this market, and was seen as an alternative to the capital intensive and inflexible way that corporations purchased hardware from the likes of Oracle and IBM for their owned and operated data centres. AWS quickly grew the market and its revenue from $12b in 2016 to the $100b run rate business today. Microsoft and Google have since entered the market and provide strong alternative offerings. The total addressable opportunity suggests multiple players can win, with 85% of IT infrastructure spend still on-premise.

Amazon’s Competitive Position

We explore the extent and durability of Amazon’s competitive advantages using Hamilton Helmer’s 7 powers:

1. Scale economies – evident across infrastructure (1,363 logistics facilities), customer and supplier base (85% US household penetration and >1m sellers) and gross merchandise sales of >$700b. Scale enables greater buying power during supplier contract negotiations, and also brings unit economics down as a large portion of the company’s cost base is fixed. This reduces a range of costs on a per unit basis, which creates significant advantages over other players. Scale in AWS is reflected in the $100b+ revenue run-rate business, strong margin profile and 125 data centres across 39 regions.

2. Network economies – taken effect across Prime and its marketplace of buyers and sellers. As Amazon’s user base grows, more suppliers are willing to sell on Amazon, thereby driving increased selection and lower prices which attracts more users. This flywheel effect is clear in the US, with profits from the >1m sellers and >100m Prime members being used to further expand and improve the value proposition while driving retention as other platforms are comparatively less attractive. In less penetrated markets, Amazon is trying to deliver the same network effect, however, remain at an earlier stage with a lower user and supplier base.

3. Counter positioning – Amazon is the leading Ecommerce player disrupting traditional brick and mortar retailers, with share of adjusted retail sales around 20%. The company has an online model that is counter-positioned against incumbents through fast-delivery, low prices and a broader selection. Although, Amazon is facing stiff competition from Chinese dropship players such as Shein, Temu and AliExpress who offer an alternative model with lower prices on lower value items by shipping direct from manufacturer. For AWS, cloud infrastructure is disrupting the traditional on-premise data centre model with a cost effective and flexible alternative that enables the ramping of compute requirements.

4. Process Power – highly automated systems across logistics that enables fast and efficient delivery. Amazon has accumulated 25 years of know-how and capex building a leading network and then effectively doubling this during COVID. The time and investment required to replicate this IP is significant. Amazon is delivering a similar infrastructure rollout across Cloud computing while also having the most extensive capabilities and broadest services on AWS.

5. Switching costs – retail is an industry with historically low switching costs. Amazon has improved repeatability on its platform through Prime membership with benefits across shipping, grocery, video, music, gaming and photos. The value proposition far outweighs the annual cost of around US$139. Amazon has increased Prime membership prices with minimal churn. For AWS, switching costs are moderate-high due to the requirement to rewrite and move workloads to another provider which may not have the same level of functionality and capability.

6. Brand – good brand image with a customer first mentality. They are known for innovation and driving better outcomes for customers which has built trust along the way.

7. Cornered Resource – the long-term orientated and high-performance culture creates an owner’s mindset that has enabled Amazon to drive innovation. New market creating innovations include AWS, Prime, Alexa and Kindle. Its remuneration framework encourages this by awarding employees with long-term stock grants that vest over 5 years or more.

1. How long can Amazon grow for in Ecommerce?

In the US, Amazon is the outright market leader with 40% market share. There are no pure-play, technology led players with scale. Its nearest competitors are Walmart and eBay that have 7% and 3% share respectively.

Ecommerce adoption has grown from 7% in 2011 to 22% in 2023. Amazon has led this growth and entered higher penetrated categories such as books & magazines (46%), consumer electronics (57%) and office supplies (56%) at an earlier stage. This along with other categories including Consumer packaged Goods and Furniture (12%), Appliances and Equipment (17%) have further room to shift online as friction reduces. Amazon already has 85% of US households as customers on Prime, with the opportunity now to monetise users further over time.

Longer term penetration can grow to 40% levels as benefits across convenience, affordability and selection become increasingly superior to bricks and mortar. This has been demonstrated in highly penetrated Ecommerce markets such as China (46%) and South Korea (35%) where competition, digitally native consumers and dense populations has supported strong market growth. These nations provide a solid barometer of where Ecommerce can get to, further validating the long runway before the sector becomes mature.

My estimates have US Ecommerce penetration growing by 75 basis points annually to 26% in FY28. This reflects market growth of 7%, above retail sales growth of 4%. Amazon can grow around 2% faster at high-single digit levels, and deliver this growth for the next decade.

There is a more profound opportunity in International markets to increase penetration and market share. The below graph highlights this and shows that Germany is the only nation where both market share and penetration is higher than the US. The company has a proven model and existing IP they can leverage in these markets. Amazon should continue to compound revenue faster and longer in International markets; by growing share, increasing Ecommerce penetration and via an emerging middle class that increases consumption.

2. What does Generative AI mean to AWS?

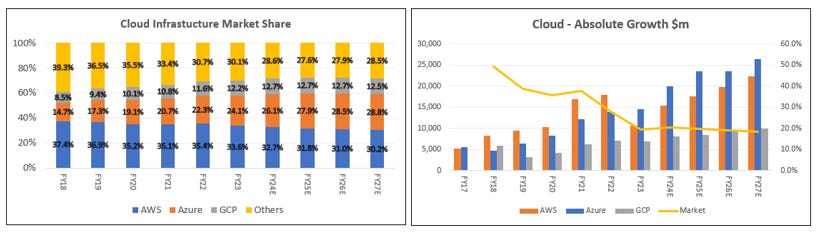

AWS is the cloud infrastructure market leader having differentiated through scale and IP across its extensive product capabilities and deepest partner network. However, since 2022, the company has come under pressure with greater market share losses from Microsoft (Azure) and Google (GCP) due to the shift to multi-cloud and customer cost optimisations.

The more recent impact is generative AI, which has shifted the leadership dynamics away from AWS to Azure through its Open AI partnership. Customers are seeking more than a partner that can handle migrations but also drive material efficiencies through AI. While Amazon has its Bedrock AI platform, Anthropic partnership and a history of leading innovation, it will take time to bring a capability that can match others. The company should continue to lose share in the near term.

Despite this, the cloud infrastructure market remains immature with 85% of workloads still on-premise. The ramp in generative AI workloads also improves market growth rates as these algorithms require significant amounts of compute. My estimates reflect some conservatism with the industry delivering 20% CAGR to FY27, while AWS grows at high-teens.

3. What happens to Amazon’s margins?

Amazon is experiencing a mix-shift to higher margin segments; advertising (40%+ margins) and AWS (30%+). Advertising has accelerated from 2% of revenue in 2017 to 11% in 2027. Assuming a 1% yearly improvement in advertising operating margins suggests NA retail margins do not reach peak 2018 levels of 2.3% until 2025. This is despite the notable scale efficiencies and cost optimisation program Amazon has undertaken across its retail fulfilment network. In comparison, industry retail margins at Costco, Walmart and Target range from 3% to 6%, implying the retail business is under earning and has potential to lift further over time.

The same mix shift is occurring Internationally, with retail margins not becoming positive until 2027.

The group level mix shift is illustrated below, which illustrates the growth in AWS, Advertising and third-party (3P) revenue and the resulting group leverage with operating margins rising from 2% in 2022 to 14% in 2027.

Management and Positioning

The key shareholders are Jeff Bezos (9% shares) as well and index funds such as Vanguard (7%) and Blackrock (6%). Management has been refreshed since 2021, with a high number of senior executives leaving the organisation to pursue other endeavours. Culture is high-performing and long-term orientated, underpinned by the incentive structure that exhibits a low base salary, no annual bonus and stock-awards with vesting terms of five years and more.

Valuation

Amazon remains the highest quality Ecommerce player globally, with a dominant share in NA and long runway ahead. The company trades favourably against other platforms from a P/E and EV/EBIT perspective, excluding the Chinese players.

The group’s valuation multiples have declined materially in conjunction with improving sales and profitability. While the premium multiple is maintained, the gap has reduced in recent years. See below.

Amazon trades on a forward P/E of 37x and can compound earnings annually at 34% to FY27. If this growth is achieved, Amazon trades on a FY27 P/E of 20x, and is a business that still has growth prospects and margin upside.

Risks to view

The counter view is that Amazon is becoming a lower growth business while competition will impact margins. Also, AWS is the number three player in Generative AI and could meaningfully lose share.

· Generative AI – as discussed Microsoft and Google are ahead in Generative AI, with AWS instead pursuing a platform-based strategy rather than owning its own solution. We could see further technological advances that make AWS less competitive. AWS has a history of innovating and the management team understands this risk, reflected in its $4b investment in Gen AI start-up Anthropic.

· Competition – the company consistently faces new threats, recently with Chinese dropship player Temu. Temu offers low-cost products at 20-40% the price of Amazon with 1-2 week delivery times. While its unit economics are negative and the venture is loss-making, Temu’s strategy has been to take share and drive customer acquisition. These dropship players are a threat, however, they mainly challenge in lower value items which are highly discretionary and have less impact on Amazon’s bottom line.

· Anti-trust – could see negative regulation around Amazon’s dominant market positions in Ecommerce and Cloud. We have seen increased regulatory scrutiny around anti-trust, data privacy breaches and tax. In the US, the Federal Trade Commission (FTC) has raised cases alleging Amazon’s use of monopolistic power via price fixing arrangements between Amazon and third-party sellers. These risks are material, although we are unlikely to see Amazon’s dominance broken up, rather the company could be subject to fines and increased scrutiny.

· Recession – while Amazon is diversified and more concentrated towards non-discretionary categories, an economic slowdown would impact the business. Retail sales could slow or fall. Cloud computing is also exposed to business growth, and a reduction in cash flows would slow growth.

Disclaimer: All posts on “cosmiccapital” are for informational purposes only. This is NOT a recommendation to buy or sell securities discussed. Please do your own work before investing your money.